Executive Summary: Key Takeaways on Mini-Loans

– Fenqile’s (分期乐) mini-loans often carry effective annual percentage rates (APRs) nearing 36%, far exceeding China’s regulatory cap of 24%, through hidden fees like membership and担保费 (guarantee fees).

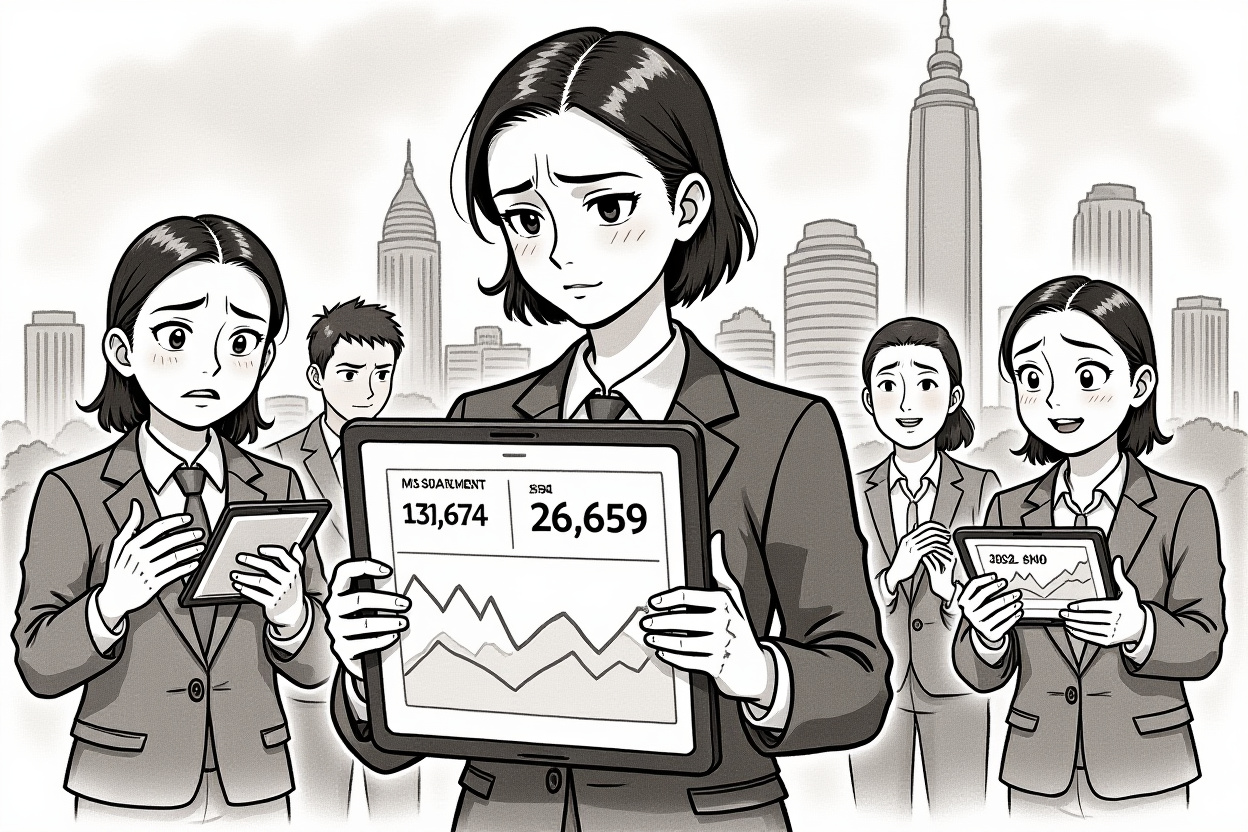

– The business model targets young and student borrowers with low monthly payments but long terms, leading to debt snowballing where small loans double in repayment amount, as seen in the case of Ms. Chen (陈女士) borrowing 13,674 yuan to repay 26,859 yuan.

– Despite regulatory efforts like the People’s Bank of China (中国人民银行) and National Financial Regulatory Administration’s guidance to cap costs, enforcement remains challenging, with platforms exploiting loopholes in fee structures and data privacy.

– Aggressive debt collection tactics, including通讯录爆裂 (contact list bombing) and harassment, coupled with invasive data harvesting, raise severe consumer protection and ethical concerns for fintech lenders like Lexin Group (乐信集团).

– Investors and regulators must scrutinize the sustainability of mini-loan models as China tightens oversight, impacting market stability and financial inclusion for vulnerable groups.

The Hidden Crisis in China’s Consumer Credit Market

As Chinese consumers gear up for festive spending during holidays like Lunar New Year, the temptation of quick cash through mini-loans has never been higher. Platforms like Fenqile (分期乐) promise easy access with slogans such as “borrow up to 200,000 yuan at rates as low as 8% APR,” but beneath this veneer of affordability lies a debt trap that is crippling a generation. The focus on mini-loans—small, short-term credit products marketed for everyday needs—reveals a systemic issue where borrowers like Ms. Chen (陈女士) find themselves repaying nearly double their principal due to opaque fees and exorbitant interest. This article delves into the mechanics of these mini-loans, their regulatory environment, and the broader implications for China’s fintech sector and global investors. With over 160,000 complaints on platforms like Hei Mao投诉 (Black Cat Complaint Platform), the urgency to address these practices cannot be overstated.

Opaque Fees and Snowballing Debt: The True Cost of Mini-Loans

Case Study: From 13,000 to 26,000 Yuan—A Borrower’s Nightmare

The viral story of Ms. Chen (陈女士) highlights how mini-loans can escalate into financial ruin. During her university years, she borrowed five loans totaling 13,674 yuan from Fenqile (分期乐) for日常消费 (daily expenses), including a 400-yuan purchase stretched over 36 months. The advertised “low interest” and “monthly payments as low as 18.23 yuan” masked APRs ranging from 32.08% to 35.90%. By 2022, she defaulted, and after over 1,000 days of逾期 (delinquency), her debt ballooned to 26,859 yuan—接近本金的两倍 (nearly double the principal). This case is not isolated; reports from The Chinese Consumer (《中国消费者》) document similar instances where borrowers faced actual repayments exceeding contracted amounts by thousands of yuan due to hidden charges.

How Fee Structures Inflate Effective APRs Beyond 24%

Mini-loans often appear affordable through extended terms, but附加条款 (additional clauses) embed costs that push综合融资成本 (comprehensive financing costs) to the legal极限 (limit). For example, Fenqile (分期乐) has been accused of charging会员费 (membership fees),信用评估费 (credit assessment fees), and担保费 (guarantee fees) without transparent disclosure. On Hei Mao投诉 (Black Cat Complaint Platform), users report that these fees, buried in lengthy电子协议 (electronic agreements), elevate APRs to 36%, violating the 24% cap set by regulators. A 2025 guidance from the People’s Bank of China (中国人民银行) and National Financial Regulatory Administration mandates a phased reduction to four times the 1-year Loan Prime Rate (LPR), but platforms continue to innovate ways to maintain profitability. This opacity not only harms borrowers but also erodes trust in China’s rapidly growing fintech ecosystem.

Regulatory Landscape: Bridging the Gap Between Policy and Practice

The 24% Cap and LPR-Based Limits: A Work in Progress

Enforcement Challenges and Consumer AdvocacyTargeting the Vulnerable: The Lingering Shadow of Campus LendingFenqile’s Origins and the Legacy of Student Debt

Aggressive Data Harvesting and Privacy ViolationsBusiness Model Scrutiny: Profitability Versus Ethical LendingThe Economics of Mini-Loans: Volume Over Value

Debt Collection Practices and Market BacklashMarket Implications and Forward-Looking GuidanceInvestor Risks in Fintech and Chinese Equities

The Future of Consumer Credit and Regulatory EvolutionSynthesizing the Mini-Loan Dilemma: A Call to ActionThe investigation into Fenqile’s (分期乐) mini-loans reveals a pervasive issue where accessible credit morphs into debilitating debt. Key takeaways include the critical need for fee transparency, stronger enforcement of existing caps, and ethical reforms in data and collection practices. For young borrowers, vigilance is paramount—scrutinize loan terms, calculate true APRs, and leverage consumer protection resources. Regulators must enhance monitoring of digital platforms and close loopholes that allow hidden fees. Investors should assess fintech firms not just on growth metrics but on compliance and social impact. As China’s economy evolves, mini-loans can either become a tool for financial inclusion or a catalyst for crisis; the choice hinges on collaborative action from all stakeholders to foster a healthier credit ecosystem.